PlanB

a3b0ce…54ad15planb@planbtc.com

793Followers0Following62Notes

Creator of the stock-to-flow model

62 total

PlanB768d ago

PlanB768d agoAdding 2% bitcoin to a classic 60/40 portfolio vastly improves performance. But most investors are too focused on Sharpe-ratio (based on st.deviation). They see that Sharpe declines a bit. Calmar-ratio (based on drawdown) is a better metric and it improves a lot! Using Calmar: ditching stocks and bonds entirely and invest 4% in BTC while holding 96% in cash, yields superior investment performance. It will take years for large traditional investors to change their risk perspective from st.deviation to drawdown and their risk/return perspective from Sharpe to Calmar. Perspective matters.

1000 sats

PlanB768d ago

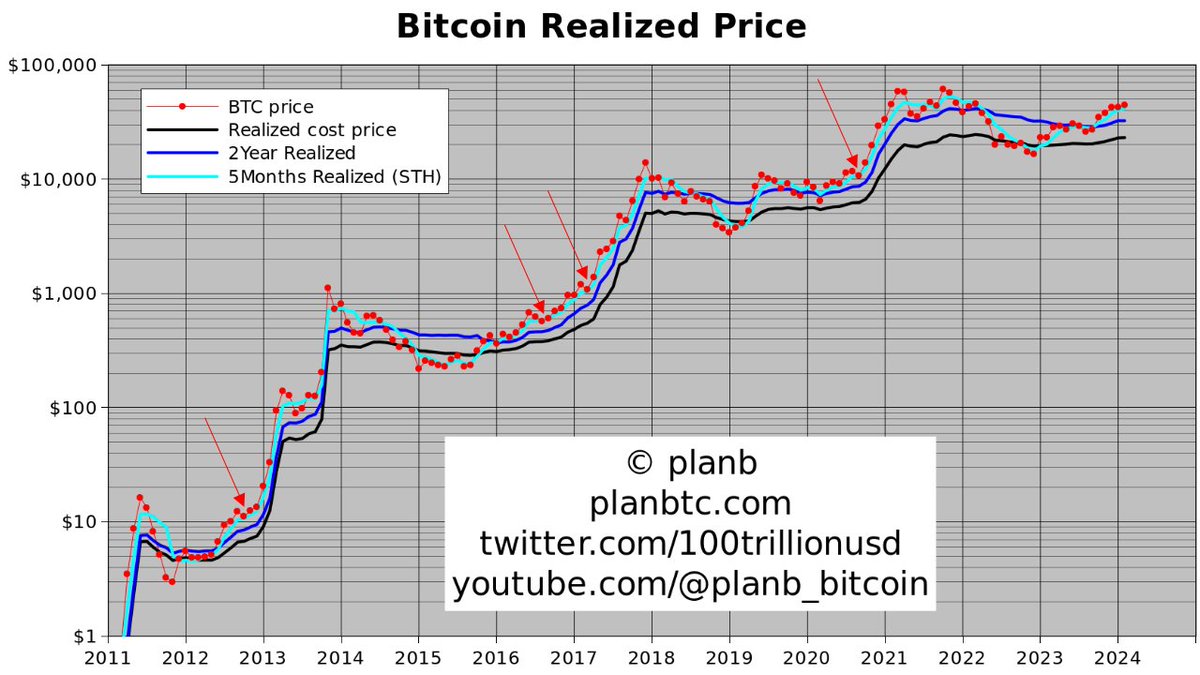

PlanB768d agoRealized prices are all increasing, and bitcoin is above them all = bullish. Also, 5M realized price (currently $40k) acts like a floor for the dips in bull markets (red arrows). So .. never below $40k again?

More info here:

https://www.youtube.com/watch?v=alEA_nqGMfI&t=407s

0100 sats

PlanB802d agoThinking of udating and reviewing these 8 charts monthly on youtube, as a short market overview.

https://youtu.be/3We9I_Cs4Cs?si=5lP6FVvT91vEuJhp

0000 sats

PlanB828d agoNew YouTube video: planB monthly market update

https://youtu.be/axMgJxZH-5s?si=Y-IJeFWsVyeZ2Hrh

0000 sats

PlanB936d agoHumans will not change (greed&fear) -> cycles will not change:

https://youtu.be/1kogTNTeOkQ

0000 sats

PlanB962d ago

New PlanB video! "Price is what you pay, value is what you get". $100k - $1m bitcoin?

https://youtu.be/iuf69tureKc

0000 sats

PlanB975d agoBitcoin $40,000-%50,000 at April 2024 halving? New planB video:

https://youtu.be/vmIlDbTgFYs

0000 sats

PlanB1018d ago

PlanB1018d ago

Bitcoin Realized Return is positive (green) for the 5th month in a row. Average cost price of May sellers was $24.6k

0200 sats

PlanB1021d ago

Some think S2F model is invalidated/broken because EMH, laser eyes, demand, autocorrelation, 100k, cointegration

Others are watching S2F trading rule and waiting for 2024 halving to bring profits once again (like 2012, 2016, 2020 halvings did before)

Time will tell who is right

0000 sats

PlanB1040d ago@dave can you please make this Python code faster (data file d.txt is ~350GB and the code processes ~2 billion dictionary inserts and ~2 billion pops)?

d={}

with open('d.txt','r') as f:

for l in f:

v=l.split(" ")

b,i,o=int(v[0]),int(v[1]),int(v[2])

for x in range(4+i,4+i+o):

d[str(v[x+o])]=(b,float(v[x]))

for x in range(4,4+i):

d.pop(str(v[x]), None)

print(d)

0100 sats

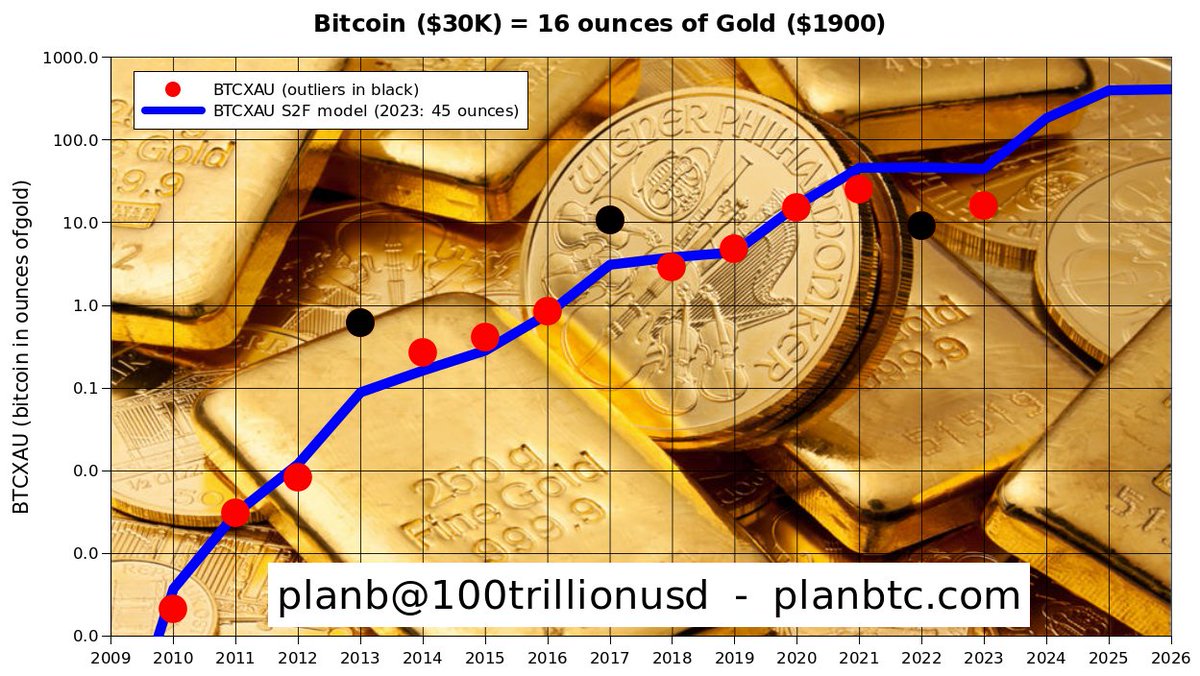

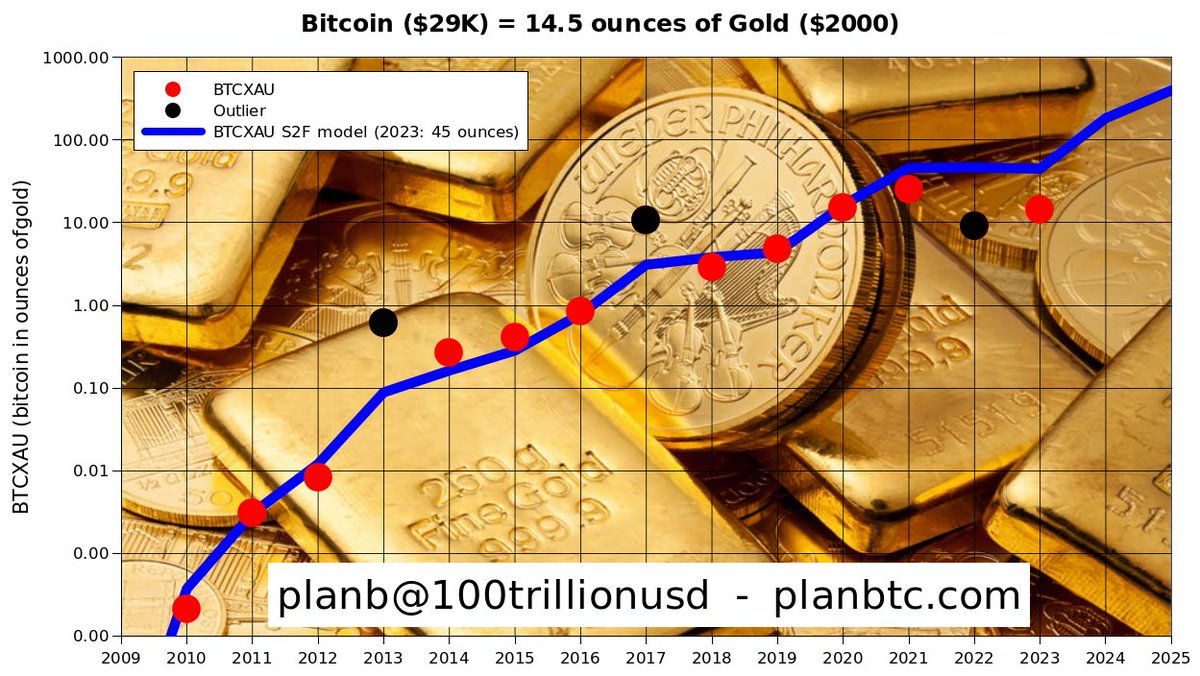

PlanB1056d ago

Let's take USD out of the equation.

Bitcoin (BTC) priced in ounces of gold (XAU).

Will 2023 be another outlier or revert to model?🔥

0000 sats

PlanB1057d ago

S2F 55k 100k and 288k models explained in this video:

https://youtu.be/DMe8_hZP98o

0000 sats

Network

Following